Canadian home sales fell to the lowest in more than five years in April, as tougher mortgage qualification rules deterred buyers.

The number of homes sold last month declined 2.9 percent from March, the Canadian Real Estate Association said Tuesday from Ottawa. Declines were recorded in about 60 percent of cities tracked including Vancouver, Calgary, Toronto and Montreal.

It was a disappointing start to the busy spring selling season for realtors that suggests markets are still struggling with tougher rules that require borrowers to prove they can afford to cope with higher interest rates. Policy makers made the changes along with other steps, such as foreign buyers taxes, to put the brakes on a surge in price gains last year that some fear could be a danger to the financial system.

The drop in April is the third monthly decline this year, with sales down over 20 percent since December. The new mortgage qualification rules kicked on Jan. 1.

Top 5 Canadian Stocks To Invest In 2019: Wells Fargo & Company(WFC)

Advisors' Opinion:- [By Motley Fool Staff]

Wells Fargo and Company (NYSE:WFC)Q1 2018 Earnings Conference CallApril 13, 2018, 10:00 a.m. ET

Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks:Operator

- [By Chris Lange]

Wells Fargo & Co. (NYSE: WFC) short interest shrank to 31.68 million shares from the previous reading of 35.77 million. Shares were trading at $52.10, within a 52-week range of $49.27 to $66.31.

- [By Lee Jackson]

Though this large cap bank is a solid value play for 2018, it still faces the possibility of large fines.�Wells Fargo & Co. (NYSE: WFC) is a�nationwide, diversified, community-based financial services company with $1.8 trillion in assets. The company provides banking, insurance, investments, mortgage and consumer and commercial finance through 8,700 locations, 12,800 ATMs, the Internet and mobile banking. It also has offices in 36 countries to support customers who conduct business in the global economy. Wells Fargo serves one in three households in the United States.

- [By Garrett Baldwin] Earnings season will kick into high gear today with the release of multiple reports from three of the nation's top financial institutions. JPMorgan Chase & Co. (NYSE: JPM), Wells Fargo & Co.�(NYSE: WFC), and Citigroup Inc. (NYSE: C) will all be in the spotlight today. U.S. President Donald Trump could be shaking up trade policy. However, it isn't NAFTA or tariffs with China that are headlining the story. According to reports, Trump has requested his advisors explore American reentry into the Transpacific Partnership (TPP). President Trump pulled the United States out of TPP shortly following his inauguration. The recommendation comes after lawmakers from ag-producing states discussed the impact of leaving the deal with the administration. The decision to reenter the TPP would be very valuable to states that produce the bulk of U.S. wheat given that it would allow exporters to avoid tariffs of $65 per tonne to Japan, which is the largest export market for American wheat. Leading nations of the pact, such as Japan and Australia, reacted coolly to the president's pivot but did not rule out the possibility of American reentry. Facebook Inc. (Nasdaq: FB) is still in focus across the financial world. Facebook CEO Mark Zuckerberg appeared before Congress two times this week to address his firm's ongoing data scandal involving consulting firm Cambridge Analytica. Congress' failure to understand how the Internet works and Facebook's business model was on full display, but Zuckerberg was able to maintain his composure as he answered questions over the two-day period. Stocks to Watch Today: JPM, WFC, C Shares of JPMorgan Chase & Co. (NYSE: JPM) are in focus as the bank prepares to report Q1 earnings before the bell. JPM stock added 1.1% despite falling short of profit expectations. Wall Street anticipated that the firm would report earnings per share (EPS) of $2.28 on top of $27.53 billion in revenue. The firm reported EPS of $2.26; however, it reported

- [By Ethan Ryder]

Shares of Wells Fargo (NYSE:WFC) have received a consensus rating of “Hold” from the twenty-nine research firms that are currently covering the firm, Marketbeat.com reports. Six investment analysts have rated the stock with a sell recommendation, seven have given a hold recommendation and sixteen have given a buy recommendation to the company. The average 12 month target price among brokers that have issued ratings on the stock in the last year is $61.86.

- [By Matthew Frankel]

It's been an eventful week in the financial markets. Wells Fargo's (NYSE:WFC) scandals are in the headlines (again), the two largest investment banks reported excellent earnings, and there's another data breach consumers should know about.

Top 5 Canadian Stocks To Invest In 2019: NRG Energy Inc.(NRG)

Advisors' Opinion:- [By Ethan Ryder]

DTE Energy (NYSE: DTE) and NRG Energy (NYSE:NRG) are both utilities companies, but which is the superior investment? We will contrast the two businesses based on the strength of their earnings, institutional ownership, profitability, valuation, risk, dividends and analyst recommendations.

- [By Jon C. Ogg]

NRG Energy Inc. (NYSE: NRG) was started with a Buy rating and�assigned a $37 price objective (versus a $33.15 close) at Merrill Lynch.

Oasis Petroleum Corp. (NYSE: OAS) was reiterated as Overweight and the target price was raised to $17 from $13 at Morgan Stanley.

Top 5 Canadian Stocks To Invest In 2019: ConocoPhillips(COP)

Advisors' Opinion:- [By Matthew DiLallo]

Oil prices have been on fire over the past year and recently topped $70 a barrel, which is the highest crude has been since late 2014. That rally in the oil market has helped fuel big-time gains in many oil stocks. Three that stand out are Anadarko Petroleum (NYSE:APC), Hess (NYSE:HES), and ConocoPhillips (NYSE:COP) because each has risen more than 20% this year. They might still have additional upside from here given that all three plan on spending billions of dollars to buy back more of their stock.

- [By Matthew DiLallo]

Shares of ConocoPhillips (NYSE:COP) continued rallying last month, rising another 10%, which put them up more than 40% over the past year. Fueling April's surge -- which added more than $7.5 billion to the company's market cap -- was a combination of higher oil prices, another oil discovery in Alaska, and strong first-quarter results.

- [By Matthew DiLallo]

ConocoPhillips (NYSE:COP) has worked hard to differentiate itself from other oil companies by focusing on creating value for investors as opposed to growing at all costs. That plan continued paying dividends during the first quarter, as the company blew past expectations. That strong showing sets the U.S. oil giant up for an exceptional year.

Top 5 Canadian Stocks To Invest In 2019: Thor Industries Inc.(THO)

Advisors' Opinion:- [By ]

Thor Industries (THO) : "They had expenses and inventory go up and it's been hurt by both. Those are negatives."

Hain Celestial Group (HAIN) : "They had a bad quarter with bad guidance. I can't reassure you here. "

- [By Logan Wallace]

Tahoe Resources (TSE:THO) (NASDAQ:TAHO) – Equities research analysts at National Bank Financial reduced their FY2018 earnings estimates for shares of Tahoe Resources in a research report issued on Monday, April 9th. National Bank Financial analyst M. Parkin now forecasts that the company will earn $0.29 per share for the year, down from their prior forecast of $0.35. National Bank Financial currently has a “Sector Perform” rating and a $8.00 price objective on the stock.

- [By ]

Cramer was bearish on Thor Industries (THO) and Hain Celestial Group (HAIN) .

Search Jim Cramer's "Mad Money" trading recommendations using our exclusive "Mad Money" Stock Screener.

Top 5 Canadian Stocks To Invest In 2019: Natural Gas(NG)

Advisors' Opinion:- [By Money Morning Staff Reports]

Canadian gold mining company NovaGold Resources Inc. (NYSE: NG) shows an even starker change in sentiment. In the last 12 months, the volume of short bets on the stock declined 79%, to 522,400.

- [By Money Morning News Team]

Canadian gold mining company NovaGold Resources Inc. (NYSE: NG) shows an even starker change in sentiment. In the last six months, the volume of short bets on the stock declined 32.75%, from 19.05 million shares to 12.81 million.

- [By Shane Hupp]

JPMorgan Chase set a GBX 870 ($11.80) target price on National Grid (LON:NG) in a research note released on Monday. The brokerage currently has a buy rating on the stock.

Source: Ford

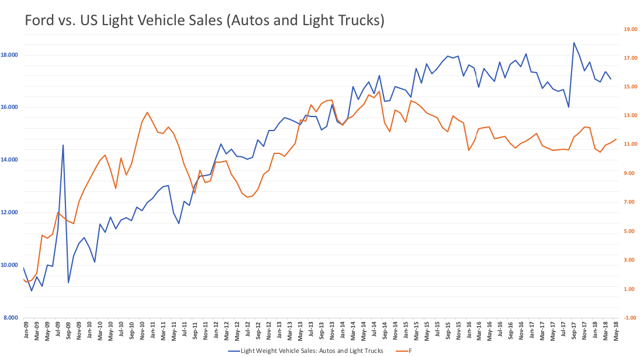

Source: Ford Source: Author's Spreadsheets (Raw Data: FRED)

Source: Author's Spreadsheets (Raw Data: FRED) Source: Ford Sales Report April 2018

Source: Ford Sales Report April 2018 Source: TradingView

Source: TradingView