Over the last few weeks we had people calling Ford (F) 'America's dumbest' company. The reasons range from the decision to focus on trucks to the death of the US consumer. I am sticking to my call that dividends will outperform capital gains but I have to refute the 'total breakdown' thesis.

Source: Ford

Source: Ford

Before I go any further, I have to mention a very important point. In April of this year, I wrote an article which mentioned an interesting mid-term opportunity. Even though my article started on a negative note I am not revising that call as I will further explain in this article.

A recent article compared the current economic environment to the one in 2005-2006. Car manufacturers shifted to trucks and SUV right before the economic crisis of 2008 given the higher demand of trucks. Since 2015/2016 we are seeing the same trend once again. Ford among others have presented investors with lower car sales and ripping truck/SUV sales almost every single month. Especially 2017 saw strong gains in the SUV and truck market.

That being said, Ford is now cutting low margin models like the Fiesta, Taurus and Fusion as I cited below.

Ford said on Wednesday the only passenger car models it plans to keep on the market in North America will be the Mustang and the upcoming Ford Focus Active, a crossover-like hatchback that's slated to debut in 2019.

That means the Fiesta, Taurus, Fusion and the regular Focus will disappear in the United States and Canada.

Ford will, however, continue to offer its full gamut of trucks, SUVs and crossovers.

- Dollar Collapse

The conclusion of the article was: ''Detroit may have handed short sellers yet another sure thing.''

The first thing I have to mention is that I am not cherry picking by referring to a website that reveals its bias in its very name. The news of Ford focusing on trucks and SUVs has been all over the internet so to speak.

Overall, I do not disagree that the current trend of rising inflation is extremely bad for the US consumer on the long run. Oil and gas prices are ripping while other key inflation indicators like housing related expenses keep their pace.

However, the reason why Ford's decision to focus on bigger vehicles is not the end of the world is because the company continues to produce the smaller vehicles in Europe for example. The technologies are ready once Ford sees the need to satisfy a rising demand of smaller vehicles. This aspect of the story is almost always ignored when people discuss Ford's decisions.

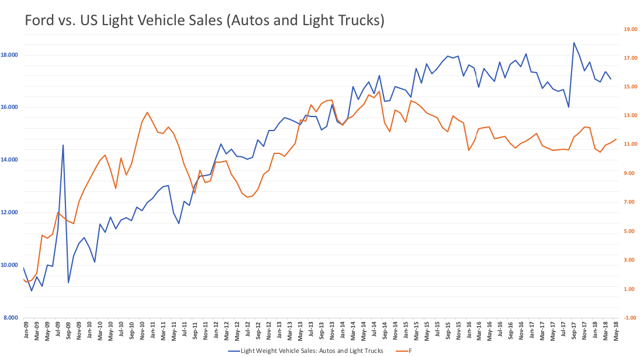

It's The Bigger Trend That CountsThe reason why Ford is not going anywhere is the auto sales peak. And by 'not going anywhere' I mean making bigger moves like the stock did in 2011 and 2012 when the US consumer celebrated its comeback.

Car sales never really made it past 18 million units per year. Sales went up from slightly less than 9 million during the GFC to 18 million in 2017.

Note that Ford peaked during the same time when sales lost their momentum. Prior to that, the company rewarded its investors with triple digit stock price returns.

Source: Author's Spreadsheets (Raw Data: FRED)

Source: Author's Spreadsheets (Raw Data: FRED)

Just last month, Ford reported a total sales decline of 4.7% which was once again led by a 15% decline among cars while trucks almost added another 1%. Especially the F-150 saw a higher ticket price which was up $900 on a month-on-month basis while F-150 sales growth has been positive for 12 consecutive month.

Source: Ford Sales Report April 2018

Source: Ford Sales Report April 2018

All of this is clear evidence of an ongoing trend from cars to trucks. Numbers like these are unlikely to occur during a recession.

That being said, it's simply not enough to turn the trend around. Investors are looking for opportunities for companies to growth their market share/sales. The current environment is simply not offering these opportunities.

What's Next?Despite the fact that expectations are low regarding Ford's sales in the US, we see favorable momentum in the retail industry. The ratio spread between retail stocks (XRT) and long term government bonds (TLT) as displayed by the green line has gained strength over the past few weeks. Normally, this is a positive sign for Ford given that this index displays investor's expectations when it comes to the US consumer.

I am still sticking to my call that Ford is likely going to hit $12.50 on the mid-term. This move is fueled by above-average economic sentiment and returning strength in the US retail industry.

Source: TradingView

Source: TradingView

However, I am also sticking to my call that the long term is looking less favorable. No, Ford is not going bankrupt and it is also not missing any technological trends. Even the focus on trucks is not going to end this company's long history.

The simple problem is that car sales have peaked. And it is extremely unlikely that late-cycle growth is going to push these numbers higher. If you are long Ford as a dividend investor I advise to stay long. Enjoy your dividend but make sure that your exposure is not too large given the cyclical nature of this company. Mid-term traders (like me) should stick to the company and start selling around $12.5 as this is a point which might see increasing resistance.

Stay tuned!

Thank you for reading my article. Please let me know what you think of my thesis. Your input is highly appreciated!

Disclosure: I am/we are long F.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article serves the sole purpose of adding value to the research process. Always take care of your own risk management and asset allocation.

No comments:

Post a Comment